Case study: using rolling planning to achieve consistent annual IT planning

In this article, we want to use a specific case study to show how much knowledge can be gained, and therefore how much money can be saved, when annual IT planning and rolling planning go hand in hand.

Rolling annual IT planning

One time is not enough or consistency is key – you’ve probably heard it a thousand times. If we use phrases that seem like calendar sayings today, it’s because they can easily be applied to your IT portfolio management. As if you want to be successful, you need a good overview and consistent planning gives you an excellent overview.

But how do we ensure that your annual planning is consistent? Quite simply, you can achieve consistent annual IT planning with the help of rolling planning.

Of course, you already have an annual plan that you regularly review and adjust if necessary. In this article, we want to use a specific case study to show how much insight and monetary gain can be achieved when annual IT planning and rolling planning go hand in hand.

Background information on the topic of IT annual planning

Let’s start at the beginning, with the project pipeline. The project pipeline is the collection point for all IT future projects in a company. It records, evaluates and prioritizes all IT actions. As a result of this process, we receive the annual plan. The project pipeline is superordinate to the annual plan, as it also contains projects that have been postponed due to prioritization. This delay is often described as an “application or project backlog”.

Evaluation of IT projects:

If an IT project is to be evaluated, the first step is to estimate the time and money required to realize the project. We have described here how such an estimate works. The basis of the estimate is the functional scope of the IT project to be realized. Therefore, at the beginning of an estimate, at least the preliminary scope of functions must be defined. In other words, there must be an idea of what the new IT product should be able to do right from the start.

Prioritize IT projects:

Once all IT projects have been evaluated, they can be prioritized in terms of when they should be implemented. The prioritization of projects is determined by the benefit that each project brings to the organization. The basis for this is the business case. Prioritization criteria are, for example, legal requirements (mandatory requirement), the optimization potential of the automated processes, sales or revenue expectations of the realized products, the discounted cash flow (DCF) or the return on investment (RoI).

IT annual planning and rolling planning

Operational planning of the IT project portfolio is carried out regularly as part of the annual planning process. It forms the starting point for action planning in the financial year and is the link between project planning and line planning. At regular intervals (monthly, quarterly), progress is compared with consumption and the budget still required. As part of the rolling planning process, the planned figures are compared with the actual figures and forecasts for the remaining budget are presented.

Case Study

This case study deals with the planning and management of the IT budget, taking financial risks into account.

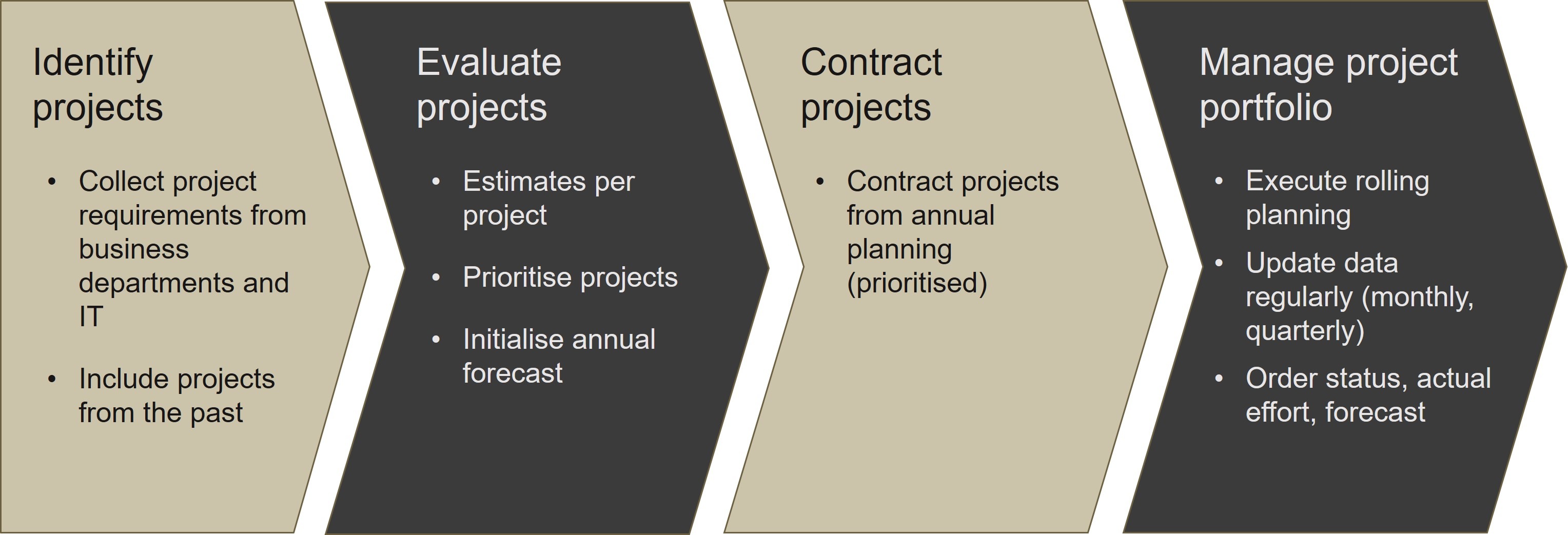

Process for planning and managing the IT project portfolio

The IT project portfolio is planned and managed on a cyclical basis. The figure illustrates this.

As already mentioned, the projects collected in the project pipeline must be evaluated and prioritized. After this step, which is often iterative, the management of your company decides which IT projects are to be realized and when.

Concrete steps

Let’s get more specific! We present an example from our practice:

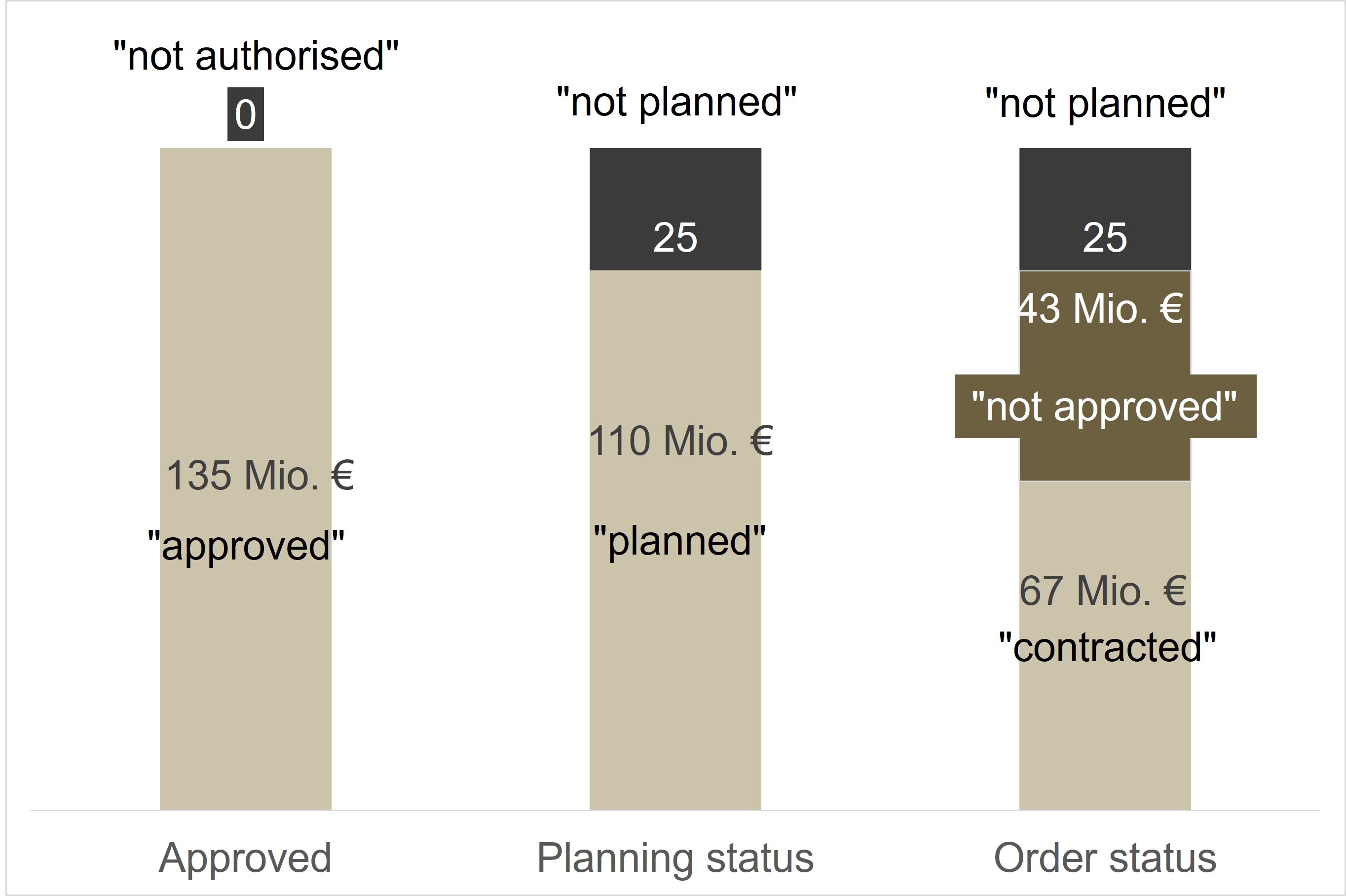

The customer has approved a development budget of EUR 135 million for 2012. Of this amount, EUR 110 million has already been planned, i.e. there is already an estimate of expenditure for IT projects amounting to EUR 110 million. Although there are projects in the project pipeline for the remaining EUR 25 million, no estimates have yet been made.

Approval by the Board of Directors is required in order to realize the evaluated projects. In this example, this has already been done for EUR 67 million of the commissioned budget for 2012 (see Figure 2).

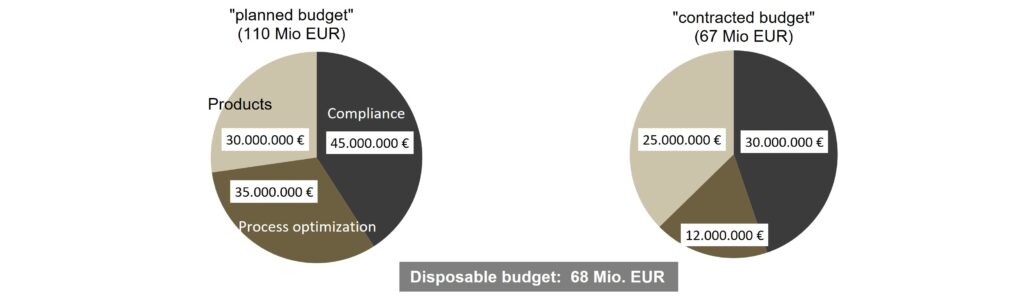

This results in a budget that is still available, also known as the “available budget”, which is made up of the “not commissioned” and “not planned” portions. In this example, its volume amounts to EUR 68 million (see Figure 3).

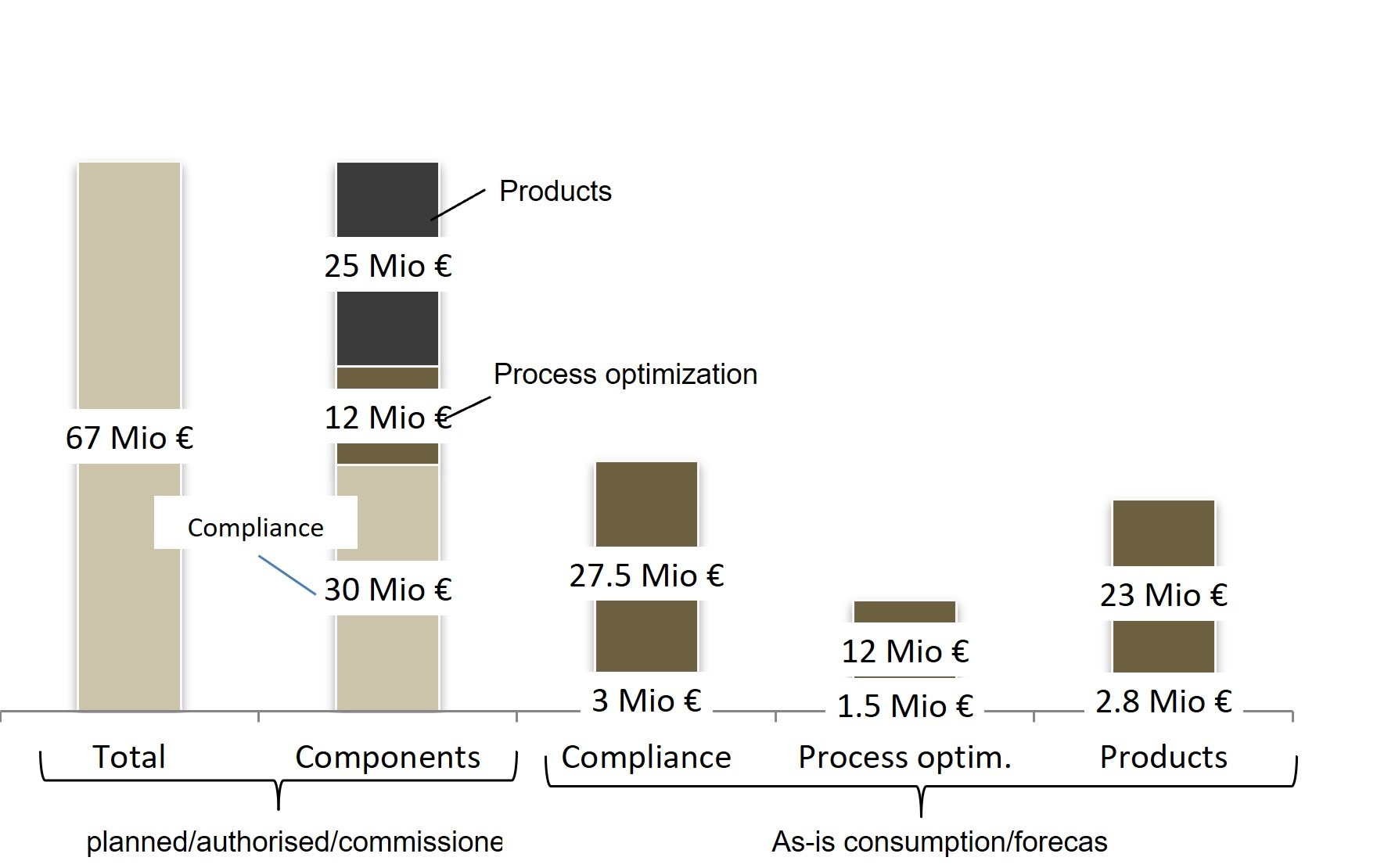

At the beginning of February, we evaluated the commissioned budget (see Figure 4) in relation to the actual expenditure and the forecast expenditure. In doing so, we referred to the key figures from January 31. Unless there was a spontaneous change, we expected that the actual expenditure together with the forecast expenditure would result in the commissioned budget. It is important to note that budget deviations can always be caused by fluctuations in productivity or creeping functional growth, known as scope creep.

Budget variances

We identified a forecast budget variance of 12.5% in the process optimization project category. The deviation in the Compliance and Products field was less than 5% and therefore did not yet trigger a reaction.

We therefore had a deviation from the commissioned budget, which led to consequences in the decision-making process (budget risk).

We also looked at the interaction with the planned budget or available budget. It turned out that the deviation could be absorbed by taking the planned budget into account. In addition, further planning reserves were available due to the unplanned budget of EUR 25 million.

Result of the analysis

The analysis of the process optimization portfolio shows that one project in particular was the main cost driver. From an initial budget of EUR 500 thousand and 150 FPs, the budget had to be increased to EUR 1.5 million by correcting the scope of functions and lower productivity.

Advantages of rolling annual IT planning

The case study provided several insights.

Firstly, it has shown how easy it is to determine the right key figures for decision-making. Secondly, we have seen how quickly IT projects can increase in scope and, accordingly, in financial and time expenditure. The cost increase of EUR 500 thousand to EUR 1.5 million is a tripling of the originally planned monetary expenditure. In the case study presented, a budget was available for this. However, this is not always the case. This is the third advantage of combining annual IT planning with rolling planning:

You get a head start. This is because you will not only find out that an IT project is significantly driving up costs at the next quarterly or annual planning stage, but much earlier. This allows you to make decisions more quickly on how to deal with them. You maintain an overview and therefore have the key to success in your hands.

Further articles can be found here:

Case Study – Life cycle costs of IT products

IT project portfolio management – keep an overview!

Case Study – Make or Buy – The first glance can be deceptive!

Case Study: Increase the predictability of IT development projects!

About the author

Categories of this post

Further interesting posts.

In IT benchmarking, we compare the performance of your company’s IT services with those of another. The aim is to identify optimization potential and derive recommendations on how to improve performance in your company.

This article presents an initial case study from IT product portfolio management, more precisely from the area of IT product cost development. The example core question is:

How are the costs of the IT product for Change and Run developing?

You have identified and evaluated your IT projects within your IT project portfolio and are now asking yourself the question: Can’t it be done more cheaply?

In this article, we use a case study from our practice to show you what cost optimization within the IT project portfolio can look like.

What is the IT value contribution? What do we mean by this and what benefits do we achieve by using it? – an introduction.